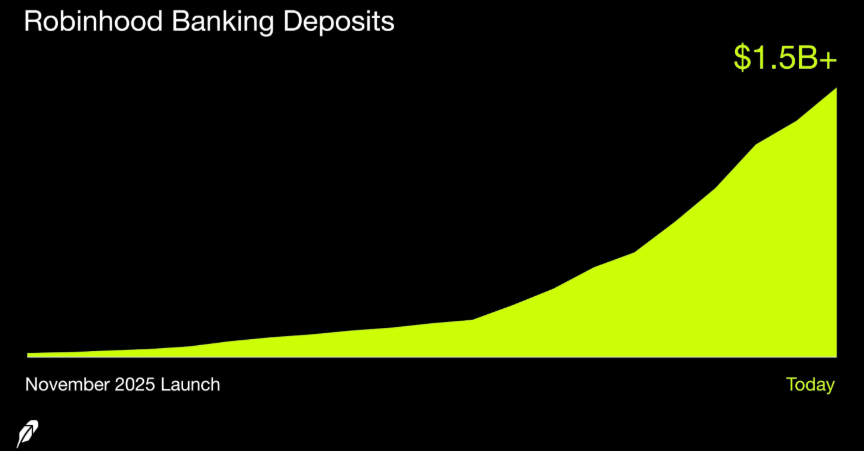

The fintech sector is undergoing a massive shift. Robinhood Markets (HOOD) CEO Vlad Tenev recently announced that Robinhood Banking has surpassed $1.5 billion in deposits — a milestone that underscores just how rapidly the platform is reshaping the competitive landscape of consumer finance.

The figure was reached with nearly 100,000 funded accounts. Deposits surged 50% in just three weeks — a growth rate that few traditional banks could match, let alone a product launched just months ago.

Robinhood Banking launched in November 2025, exclusively for Robinhood Gold subscribers. The product offers FDIC-insured checking accounts and a high-yield savings option powered by Coastal Community Bank — giving users access to competitive returns without leaving the Robinhood ecosystem.

The growth trajectory is striking. In December 2025, Robinhood Banking held just $100 million in deposits. By January 2026, it had generated $300 million with 20,000 customers. By early March, deposits crossed $1 billion across 65,000 accounts. The latest data shows deposits nearly doubled in under a month.

Perhaps the most telling data point: the average deposit per customer sits at $15,000. That figure suggests users are not just experimenting with the product — they are moving their primary banking relationships to Robinhood. Tenev's broader ambition is clear: build a unified financial Super App encompassing stocks, options, crypto, credit cards, and retirement accounts. In 2025, Robinhood recorded $68 billion in net deposits and reached 4.2 million Gold subscribers.

While Robinhood accelerates, Coinbase remains structurally exposed. Coinbase does not offer checking accounts or FDIC-insured savings. Its liquidity features rely on USD balances for trading and USDC yields tied to Coinbase One subscriptions. By contrast, Robinhood guarantees FDIC coverage up to $2.5 million per depositor through its sweep program — a significant structural advantage in the battle for everyday consumer banking.

Coinbase's stablecoin operations generated $1.35 billion in revenue in 2025, up from $911 million the prior year. But that revenue stream faces regulatory headwinds. The GENIUS Act, signed in July 2025, prohibits stablecoin issuers from paying interest to holders. Meanwhile, the CLARITY Act — still under Senate review — could further restrict Coinbase's ability to offer USDC rewards. These legislative developments add meaningful uncertainty to one of Coinbase's fastest-growing revenue lines.

Both companies are racing toward the same destination — a financial Super App — but from opposite directions. Robinhood started with equities and layered in credit, crypto, and banking. Coinbase started in crypto and added 24/7 stock trading. The strategic convergence is unmistakable — the question is who captures the consumer relationship first.

Markets responded positively to Tenev's deposit milestone announcement. HOOD stock rose 6.35% on March 30. While the stock remains roughly 40% below its all-time high of $152.46 set in October 2025, it is still up approximately 85% year-over-year — suggesting the market sees long-term value in Robinhood's Super App trajectory.

The Demographic Advantage

Robinhood holds a structural edge that often goes underappreciated: 75% of its 27 million users are under 44 years old. This young user base positions Robinhood exceptionally well for the long-term battle for daily financial engagement. Coinbase, by contrast, has not grown its monthly active user count since 2021, with revenues remaining tightly correlated to crypto market volatility. As Coinbase navigates stablecoin regulatory uncertainty, Robinhood is quietly locking in the next generation of banking customers.